16-month CD

A 16-month CD (Certificate of Deposit) is a type of savings account offered by banks and credit unions. Here are the key characteristics:

- Fixed Term: It has a maturity period of nine months, during which the deposited money is locked in.

- Interest Rate: Typically offers a fixed interest rate generally higher than regular savings accounts.

- Minimum Deposit: Often requires a minimum deposit amount to open the account.

- Early Withdrawal Penalty: If you withdraw the funds before the 16-month term ends, you usually incur a penalty, a portion of the interest earned, or a specified fee.

- FDIC Insured: In the United States, CDs from credit unions are usually insured by the National Credit Union Administration (NCUA) up to $250,000 per depositor per credit union.

A 16-month CD can be a good option if you have a specific short-term savings goal and want to earn a higher interest rate without taking on much risk.

A 16-month CD works as follows:

- Opening the CD: You deposit a lump sum of money into the CD account. The amount often needs to meet the bank or credit union’s minimum deposit requirement.

- Fixed Term: The money is committed to the CD for a fixed term of nine months. During this period, you cannot add to or withdraw from the principal amount without incurring penalties.

- Interest Rate: The bank or credit union pays you a fixed interest rate on the deposited amount for the entire term. This rate is usually higher than that of a regular savings account because the bank can use your money for a predictable period.

- Interest Accumulation: Interest is typically compounded and credited to your account at regular intervals, such as monthly or quarterly.

- Maturity: At the end of the 16-month term, the CD matures. You then have a few options:

- Withdraw the funds: You can take out your initial deposit plus the interest earned.

- Renew the CD: You can roll over the funds into a new CD, either for the same term or a different one, possibly at a new interest rate.

- Transfer the funds: You can transfer the money to another account.

- Early Withdrawal Penalty: If you need to access the money before the 16-month term ends, you will likely face an early withdrawal penalty. This penalty varies by institution but generally involves forfeiting a portion of the interest earned.

- FDIC/NCUA Insurance: If the CD is held at a bank, it is insured by the FDIC (Federal Deposit Insurance Corporation) up to $250,000 per depositor per bank. If held at a credit union, it is insured by the NCUA (National Credit Union Administration) with the same coverage limits.

A 16-month CD can be a suitable option for short-term savings goals, offering a balance between earning a higher interest rate and having your money tied up for a relatively short period.

Yes, your money is safe in a 16-month CD. At People Driven Credit Union, our CDs are insured by the NCUA (National Credit Union Administration) up to $250,000 per depositor.

APY stands for Annual Percentage Yield. It is a measure of the total amount of interest earned on an account based on the interest rate and the frequency of compounding over a year. APY is a useful metric for comparing the annual earnings on different savings products, such as savings accounts, CDs, and money market accounts, because it standardizes the effect of compounding.

Key Points About APY

- Includes Compounding: APY accounts for how often interest is compounded (e.g., daily, monthly, quarterly), which can significantly affect the total interest earned over time.

- Comparison Tool: APY provides a standard way to compare the annual interest earnings of different savings products, regardless of how frequently interest is compounded.

- Formula: The formula for calculating APY is:

APY = (1 + r/n)^n - 1

where r is the nominal interest rate (expressed as a decimal), and n is the number of compounding periods per year.

- Higher APY: A higher APY indicates that you will earn more interest on your money over a year, assuming the same principal amount.

Example

For example, if a savings account offers an interest rate of 5% compounded monthly, the APY would be higher than 5% due to the effect of monthly compounding. This makes APY a useful metric for comparing the real return on different financial products.

When you’re comparing savings accounts, CDs, or other financial products, you’ll often see two numbers: an interest rate (or dividend rate, if it’s a credit union account) and an Annual Percentage Yield (APY). At first glance, they might seem like the same thing—but they’re not. Knowing the difference helps you make smarter financial choices, whether you’re opening a savings account or making a long-term investment. Let’s break it down.

Interest Rate or Dividend Rate: the Base Number

Interest Rate

The interest rate is the basic percentage a bank or credit union uses to calculate how much you’ll pay on a loan or earn on a deposit, before considering how often interest is added (compounded).

Let’s say you open a credit union savings account with an interest rate of 3.00%. That’s the base rate your money earns before compounding is applied.

Dividend Rate

At a credit union, the term “dividend rate” is often used instead of “interest rate” for deposit accounts. As a member-owner, you’re technically receiving a share of the credit union’s earnings—similar to a dividend from a company. Functionally, though, the dividend rate works the same way as an interest rate on a bank account.

Annual Percentage: the Full Picture of Earnings or Costs

Annual Percentage Yield (APY)

APY shows how much you earn in a year on deposits, including the effects of compounding. Compounding is the process of earning interest on your interest (for deposits) or being charged interest on interest (for loans).

If your account compounds interest daily or monthly, you’ll earn a bit more than the base rate, because you start earning interest on the interest that’s already been added. That extra boost from compounding is why the APY is slightly higher than the interest/dividend rate.

Compounding Interest: Dividend Rate vs APY

APY provides a clearer picture of the actual annual earnings from savings accounts, money markets, and certificates because it includes compounding. For loans, APR is the more accurate number for comparing costs between offers, because it reflects compounding as well as fees.

- Interest Rate/Dividend Rate: If a savings account offers a 5% interest rate compounded monthly, the nominal rate is 5%. This is the base number for how much your balance will grow before compounding.

- APY: When considering the monthly compounding, the same account will have an APY slightly higher than 5% because the interest earned each month also earns interest in subsequent months.

Comparing Financial Offers Using APY

If you only look at the interest or dividend rate, you might think two products are equal—but differences in compounding or fees can make one clearly better for your wallet.

A savings account with a slightly lower rate but daily compounding could earn you more than one with a higher rate but annual compounding.

Interest Rate vs APY Example

Always use APY when comparing savings products from different institutions. Knowing the difference between the base rate and APY helps you see the full picture, allowing you to make confident choices—whether you’re saving for a big purchase or making long-term investments.

Let’s compare two savings accounts:

| Account | Dividend/

Interest Rate |

Compounding |

APY |

|

A |

3.00% | Annual | 3.00% |

| B | 3.00% | Monthly |

3.04% |

Both accounts have the same base rate, but because Account B compounds monthly, the APY is slightly higher. That’s the effect of compounding.

Let Us Help You With the Next Big Stage of Your Life

At People Driven Credit Union, we’re dedicated to helping you achieve your financial goals. As a member-owned financial institution, we’re literally invested in your future—and stand behind our commitment to transparency, security, and service excellence.

Become a member and open an account today!

1. How often are dividends compounded?

Dividends on savings, money market accounts, and certificates are typically compounded and credited monthly unless otherwise stated in the account disclosure. Compounding helps your balance grow by earning dividends on previously earned dividends.

2. Why is the APY higher than the dividend rate on a certificate?

The dividend rate is the base rate used to calculate earnings. APY shows what you actually earn over a year, including compounding. Because dividends are compounded, the APY is slightly higher than the dividend rate.

3. What is the difference between APY and APR?

APY applies to deposit accounts and shows how much you earn in a year. APR applies to loans and shows the total yearly cost of borrowing, including certain fees. Use APY when comparing savings products and APR when comparing loans.

4. Does compounding frequency really make a difference?

Yes. The more often dividends are compounded, the sooner you begin earning dividends on previously earned dividends. Over time, even small differences can increase your total earnings.

5. When comparing accounts, should I look at the dividend rate or APY?

APY is the better number to compare. It reflects the total amount you can expect to earn over a year, including compounding, giving you a clearer picture of your true return.

9-month CD

APY stands for Annual Percentage Yield. It is a measure of the total amount of interest earned on an account based on the interest rate and the frequency of compounding over a year. APY is a useful metric for comparing the annual earnings on different savings products, such as savings accounts, CDs, and money market accounts, because it standardizes the effect of compounding.

Key Points About APY

- Includes Compounding: APY accounts for how often interest is compounded (e.g., daily, monthly, quarterly), which can significantly affect the total interest earned over time.

- Comparison Tool: APY provides a standard way to compare the annual interest earnings of different savings products, regardless of how frequently interest is compounded.

- Formula: The formula for calculating APY is:

APY = (1 + r/n)^n - 1

where r is the nominal interest rate (expressed as a decimal), and n is the number of compounding periods per year.

- Higher APY: A higher APY indicates that you will earn more interest on your money over a year, assuming the same principal amount.

Example

For example, if a savings account offers an interest rate of 5% compounded monthly, the APY would be higher than 5% due to the effect of monthly compounding. This makes APY a useful metric for comparing the real return on different financial products.

Withdrawing money from a 9-month CD before the term ends typically incurs an early withdrawal penalty. At People Driven Credit Union, the Early Withdrawl Penalty is a Loss of 90 days of interest for withdrawing funds early.

Yes, your money is safe in a 9-month CD. At People Driven Credit Union, our CDs are insured by the NCUA (National Credit Union Administration) up to $250,000 per depositor.

When you’re comparing savings accounts, CDs, or other financial products, you’ll often see two numbers: an interest rate (or dividend rate, if it’s a credit union account) and an Annual Percentage Yield (APY). At first glance, they might seem like the same thing—but they’re not. Knowing the difference helps you make smarter financial choices, whether you’re opening a savings account or making a long-term investment. Let’s break it down.

Interest Rate or Dividend Rate: the Base Number

Interest Rate

The interest rate is the basic percentage a bank or credit union uses to calculate how much you’ll pay on a loan or earn on a deposit, before considering how often interest is added (compounded).

Let’s say you open a credit union savings account with an interest rate of 3.00%. That’s the base rate your money earns before compounding is applied.

Dividend Rate

At a credit union, the term “dividend rate” is often used instead of “interest rate” for deposit accounts. As a member-owner, you’re technically receiving a share of the credit union’s earnings—similar to a dividend from a company. Functionally, though, the dividend rate works the same way as an interest rate on a bank account.

Annual Percentage: the Full Picture of Earnings or Costs

Annual Percentage Yield (APY)

APY shows how much you earn in a year on deposits, including the effects of compounding. Compounding is the process of earning interest on your interest (for deposits) or being charged interest on interest (for loans).

If your account compounds interest daily or monthly, you’ll earn a bit more than the base rate, because you start earning interest on the interest that’s already been added. That extra boost from compounding is why the APY is slightly higher than the interest/dividend rate.

Compounding Interest: Dividend Rate vs APY

APY provides a clearer picture of the actual annual earnings from savings accounts, money markets, and certificates because it includes compounding. For loans, APR is the more accurate number for comparing costs between offers, because it reflects compounding as well as fees.

- Interest Rate/Dividend Rate: If a savings account offers a 5% interest rate compounded monthly, the nominal rate is 5%. This is the base number for how much your balance will grow before compounding.

- APY: When considering the monthly compounding, the same account will have an APY slightly higher than 5% because the interest earned each month also earns interest in subsequent months.

Comparing Financial Offers Using APY

If you only look at the interest or dividend rate, you might think two products are equal—but differences in compounding or fees can make one clearly better for your wallet.

A savings account with a slightly lower rate but daily compounding could earn you more than one with a higher rate but annual compounding.

Interest Rate vs APY Example

Always use APY when comparing savings products from different institutions. Knowing the difference between the base rate and APY helps you see the full picture, allowing you to make confident choices—whether you’re saving for a big purchase or making long-term investments.

Let’s compare two savings accounts:

| Account | Dividend/

Interest Rate |

Compounding |

APY |

|

A |

3.00% | Annual | 3.00% |

| B | 3.00% | Monthly |

3.04% |

Both accounts have the same base rate, but because Account B compounds monthly, the APY is slightly higher. That’s the effect of compounding.

Let Us Help You With the Next Big Stage of Your Life

At People Driven Credit Union, we’re dedicated to helping you achieve your financial goals. As a member-owned financial institution, we’re literally invested in your future—and stand behind our commitment to transparency, security, and service excellence.

Become a member and open an account today!

1. How often are dividends compounded?

Dividends on savings, money market accounts, and certificates are typically compounded and credited monthly unless otherwise stated in the account disclosure. Compounding helps your balance grow by earning dividends on previously earned dividends.

2. Why is the APY higher than the dividend rate on a certificate?

The dividend rate is the base rate used to calculate earnings. APY shows what you actually earn over a year, including compounding. Because dividends are compounded, the APY is slightly higher than the dividend rate.

3. What is the difference between APY and APR?

APY applies to deposit accounts and shows how much you earn in a year. APR applies to loans and shows the total yearly cost of borrowing, including certain fees. Use APY when comparing savings products and APR when comparing loans.

4. Does compounding frequency really make a difference?

Yes. The more often dividends are compounded, the sooner you begin earning dividends on previously earned dividends. Over time, even small differences can increase your total earnings.

5. When comparing accounts, should I look at the dividend rate or APY?

APY is the better number to compare. It reflects the total amount you can expect to earn over a year, including compounding, giving you a clearer picture of your true return.

A 9-month CD works as follows:

- Opening the CD: You deposit a lump sum of money into the CD account. The amount often needs to meet the bank or credit union’s minimum deposit requirement.

- Fixed Term: The money is committed to the CD for a fixed term of nine months. During this period, you cannot add to or withdraw from the principal amount without incurring penalties.

- Interest Rate: The bank or credit union pays you a fixed interest rate on the deposited amount for the entire term. This rate is usually higher than that of a regular savings account because the bank can use your money for a predictable period.

- Interest Accumulation: Interest is typically compounded and credited to your account at regular intervals, such as monthly or quarterly.

- Maturity: At the end of the 9-month term, the CD matures. You then have a few options:

- Withdraw the funds: You can take out your initial deposit plus the interest earned.

- Renew the CD: You can roll over the funds into a new CD, either for the same term or a different one, possibly at a new interest rate.

- Transfer the funds: You can transfer the money to another account.

- Early Withdrawal Penalty: If you need to access the money before the 9-month term ends, you will likely face an early withdrawal penalty. This penalty varies by institution but generally involves forfeiting a portion of the interest earned.

- FDIC/NCUA Insurance: If the CD is held at a bank, it is insured by the FDIC (Federal Deposit Insurance Corporation) up to $250,000 per depositor per bank. If held at a credit union, it is insured by the NCUA (National Credit Union Administration) with the same coverage limits.

A 9-month CD can be a suitable option for short-term savings goals, offering a balance between earning a higher interest rate and having your money tied up for a relatively short period.

A 9-month CD (Certificate of Deposit) is a type of savings account offered by banks and credit unions. Here are the key characteristics:

- Fixed Term: It has a maturity period of nine months, during which the deposited money is locked in.

- Interest Rate: Typically offers a fixed interest rate generally higher than regular savings accounts.

- Minimum Deposit: Often requires a minimum deposit amount to open the account.

- Early Withdrawal Penalty: If you withdraw the funds before the 9-month term ends, you usually incur a penalty, a portion of the interest earned, or a specified fee.

- FDIC Insured: In the United States, CDs from credit unions are usually insured by the National Credit Union Administration (NCUA) up to $250,000 per depositor per credit union.

A 9-month CD can be a good option if you have a specific short-term savings goal and want to earn a higher interest rate without taking on much risk.

Account Help

If you were a former Community Alliance Credit Union business member and used software such as QuickBooks, Quicken, or Mint, your business accounts may have required a connection update after the merger with People Driven Credit Union. The original conversion period took place in March 2023, so these instructions apply only to that legacy transition process.

Original conversion dates

March 10, 2023: Final transaction download and backup before conversion.

March 13, 2023: Deactivate and reactivate your online banking connection using People Driven Credit Union settings.

Conversion guides

QuickBooks Desktop Conversion Instructions

QuickBooks Online Conversion Instructions

Quicken Conversion Instructions

Mint Conversion Information

What to do now

If you are still having trouble with a legacy business account connection or accounting software setup, contact People Driven Credit Union for help reviewing your current account access and connection settings.

Need help?

Call 844-700-7328 or 248-263-4100 during business hours, or visit Contact Business Services.

You may not be able to make an ATM deposit because many ATM locations available to People Driven Credit Union members are withdrawal-only. In some cases, your card or account may also have restrictions that affect deposit access. If you are having trouble making a deposit, call 844-700-7328 during business hours for help.

Where you can make deposits

People Driven Credit Union no longer has traditional ATMs inside our branches. Instead, every branch drive-thru has Interactive Teller Machines, or ITMs. ITMs work like an ATM for everyday transactions, but during business hours you can also press a button to connect with a live teller for help. At an ITM, you can withdraw cash, deposit cash, deposit checks, transfer funds, make loan payments, and check balances.

Why some ATM deposits do not work

PDCU members have access to a large nationwide network of surcharge-free ATM locations, but those ATM locations are generally for withdrawals only and do not accept deposits. If you are trying to deposit cash or checks, use a PDCU branch ITM or another approved deposit method instead.

Another way to deposit checks

You can also deposit checks through the MyPDCU app. Log in to online banking or the app, select “Deposit,” enter the check amount, choose your account, and upload clear images of the front and back of the check. Be sure to sign the back and write “For Mobile Deposit Only at PDCU” along with your PDCU account number before submitting the deposit.

Need help?

If you are not sure which deposit option to use, call 844-700-7328 or contact us.

You can view your eStatements by signing in to online banking or by using the MyPDCU app. Once you are signed in, open the Statements or Documents section and select the statement you want to view or download.

How to view your eStatements online

Log in to online banking, click on the eStatements tab, choose the month or statement period you need, and open the file. You can usually view the statement on screen or download it as a PDF for your records.

How to view your eStatements in the app

Open the MyPDCU app, tap eStatements, select the account if needed, and choose the statement you want to open.

Need help?

If you cannot find a statement or need help accessing your eStatements, call 844-700-7328 during business hours. Statement history may vary by account and retention policies.

To close your People Driven Credit Union account, contact us directly by phone or visit a branch. We will verify your identity, review your account status, and help you complete the closure process.

How to close your account

Call 248-263-4100 or visit a branch to request account closure. Before the account is closed, make sure you review your current balance, pending payments, automatic withdrawals, and direct deposits. You should also transfer or withdraw any remaining funds and request confirmation once the account has been closed.

Important to know

Account closures are not handled online. If you receive direct deposit or have recurring payments tied to the account, be sure to update those with your employer, benefits provider, or billing companies before closing the account.

Need help?

If you have questions about closing your account, call 248-263-4100 during business hours, or visit a branch for assistance.

Accounts

Domestic wire transfers are usually processed the same business day if the request is submitted before the daily cutoff. In many cases, funds are available to the recipient within hours.

Actual timing can vary based on when the transfer is requested and the receiving financial institution, so contact People Driven Credit Union if you need help with a time-sensitive wire.

An ACH transfer is commonly used for everyday electronic transactions such as direct deposit, external account links, and automatic payments. A wire transfer is typically used when money needs to move more quickly, especially for larger or more time-sensitive payments.

ACH transfers and wire transfers are not the same, and they may use different instructions. If you are setting up a wire transfer, make sure you use People Driven Credit Union’s specific wire instructions instead of relying only on the standard routing number.

To send a wire transfer from your People Driven Credit Union account, call us at 248-263-4100 or visit a branch for assistance. You will need to provide the recipient’s full name, address, account number, and the receiving financial institution’s routing information.

Wire transfers are typically used for large or time-sensitive payments. Because wires are processed using specific instructions and generally cannot be reversed once completed, it is important to verify all details carefully before submitting your request.

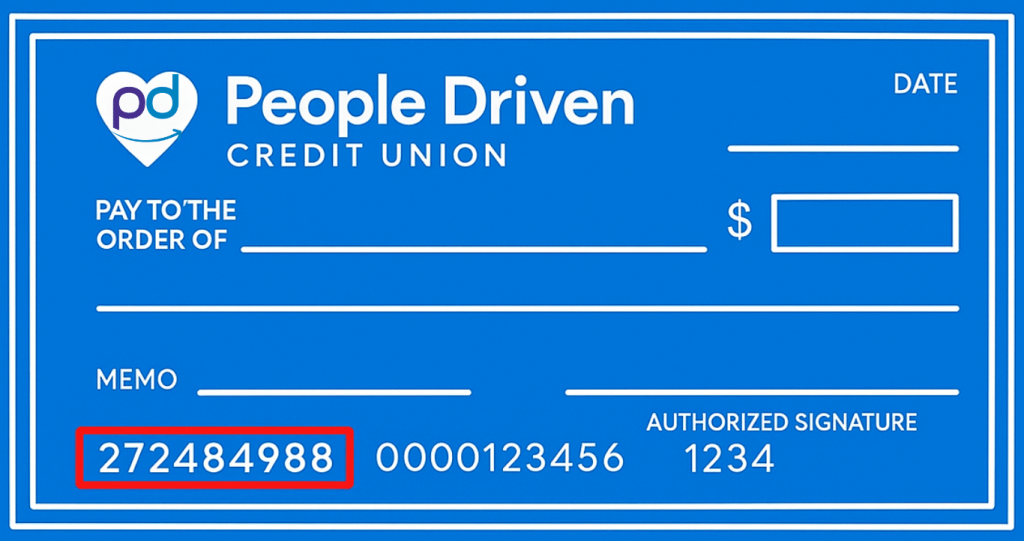

Not always. People Driven Credit Union’s routing number, 272484988, is used for direct deposit, ACH transfers, and many standard account setup requests. Wire transfers may require different instructions, depending on whether you are sending or receiving the wire.

If you are receiving a wire transfer, be sure to follow People Driven Credit Union’s specific wire instructions. If you are unsure which number to use, contact us before submitting the transfer so you can avoid delays.

Yes. You can use People Driven Credit Union’s routing number, 272484988, to link your PDCU account to an external account at another financial institution. In most cases, you will also need your account number and may need to complete a verification step, such as confirming trial deposits.

Before submitting the request, double-check that you are using the correct routing number and the correct account number for the account you want to link. Using the wrong information can delay the setup process.

Yes. You can use People Driven Credit Union’s routing number, 272484988, for direct deposit. You will also need your personal account number so your deposit is sent to the correct account.

When setting up direct deposit, make sure you provide both the correct routing number and the correct account number. If you are a former Community Alliance Credit Union member, be sure to use People Driven Credit Union’s routing number for any new direct deposit instructions.

A routing number identifies the financial institution, while an account number identifies your specific account at that institution. You may need both numbers to set up direct deposit, automatic payments, ACH transfers, or external account links.

People Driven Credit Union’s routing number is 272484988. Your account number is unique to you, so be sure to use the correct account number for the specific checking or savings account you want to use.

No. This form is a way to get started and connect with our team. We will follow up to help complete the account opening process.

Most requests can be handled quickly once we connect with you.

Yes. Use the form to tell us about your interest, and we can help you with next steps for one child or multiple children.

ACH Origination

Simply fill out the contact form below, and a PDCU Business Services representative will guide you through the setup process. You can also call us at (248) 263-4100 for assistance.

Yes. You can set up one-time or recurring payments to payees, making it easier to automate payroll, rent, or vendor payments.

PDCU’s ACH Origination includes multiple layers of security such as encrypted authentication, customizable user permissions, dual approval workflows, and automatic notifications for each ACH batch.

There’s no hard limit on the number of transactions you can initiate, but transaction volume and limits may be based on your account profile and risk review.

You can make a wide range of payments, including:

- Employee payroll

- Vendor and supplier payments

- Membership dues

- Interbank transfers

- State and Federal tax payments

ACH Origination is available to eligible People Driven Credit Union business members with an active business checking account. Our team will work with you to assess your needs and get you set up.

ACH Origination is a service that allows businesses to send and receive electronic payments through the Automated Clearing House (ACH) network. It’s commonly used for direct deposit, vendor payments, recurring billing, and tax remittances.

Nacha, short for the National Automated Clearing House Association, is the nonprofit organization that oversees the ACH (Automated Clearing House) network in the United States.

What Does Nacha Do?

- Manages the Rules: Nacha develops, maintains, and enforces the Nacha Operating Rules, which govern the processing of ACH payments and ensure consistency, security, and reliability across all financial institutions using the network.

- Ensures Security and Compliance: Nacha establishes standards for data security, risk management, and fraud prevention for organizations participating in ACH transactions.

- Promotes Innovation: Nacha works with banks, credit unions, and businesses to support new payment solutions, such as Same Day ACH and tools for faster settlement and improved access to electronic payments.

- Educates and Advocates: Nacha serves as an advocate for the ACH network, helping both financial institutions and the public understand how electronic payments work and why they’re secure and efficient.

In short, Nacha is the governing body behind the ACH network, ensuring it operates smoothly, safely, and in a way that benefits both consumers and businesses.

The Automated Clearing House (ACH) network is a secure, nationwide system that financial institutions use to transfer funds between bank accounts in the United States electronically. Managed by Nacha (National Automated Clearing House Association), the ACH network enables both credit and debit transactions, including:

- Direct deposits of payroll, Social Security, and tax refunds

- Automatic bill payments for utilities, mortgages, and loans

- Business-to-business payments

- Peer-to-peer money transfers

- Government and tax payments

ACH transactions are typically processed in batches, rather than instantly, like wire transfers, and often settle within one to two business days; however, same-day ACH is available in some cases.

It’s a cost-effective and efficient way for businesses and consumers to transfer money electronically, eliminating the need for checks or credit card networks.

Adjustable Rate Mortgage

Meet Our PDCU Mortgage Specialist

Michelle Dzon is authorized to act as an agent on behalf of People Driven Credit Union. Contact her for personalized assistance with your mortgage needs.

Michelle Dzon

Member First Mortgage

michelle.dzon@memberfirstmortgage.com

Connect with Michelle

616-301-1714 | NMLS ID: #401292

Private mortgage insurance, or PMI, is insurance that helps protect the lender if a borrower stops making payments on a conventional mortgage loan. PMI is typically required when your down payment is less than 20% of the home’s purchase price or original value.

When PMI is usually required

PMI is most commonly required on a conventional mortgage when you put less than 20% down. It increases the cost of the loan, but it may also help you qualify for a mortgage sooner if you do not have a larger down payment.

When PMI may be removed

In many cases, you can ask to remove PMI once your loan balance reaches 80% of the home’s original value and you meet the lender’s requirements. In general, PMI is automatically terminated when your loan balance is scheduled to reach 78% of the home’s original value, as long as your loan is current.

Need help?

If you have questions about PMI or your mortgage options, connect with a mortgage loan officer for personalized guidance.

Yes, many borrowers choose to refinance their ARM to a fixed-rate mortgage before the adjustable period begins to lock in a stable interest rate and predictable monthly payments.

Consider your financial situation, how long you plan to stay in the home, and your risk tolerance for potential interest rate changes. ARMs can be a good choice if you plan to sell or refinance before the adjustable period begins or expect interest rates to remain stable or decline.

Some ARMs may have prepayment penalties, but People Driven Credit Union does not. You can refinance or pay off your Adjustable Rate Mortgage with PDCU early without any prepayment penalties.

Yes, ARMs often have caps that limit how much the interest rate can increase at each adjustment period and over the life of the loan. These caps provide some protection against large payment increases.

ARM interest rates adjust based on a specific index (such as the Treasury index) plus a margin set by the lender. When the index rate changes, the interest rate on your loan adjusts accordingly.

The main risk with an ARM loan is that your monthly payments can increase if interest rates rise. Understanding the potential for payment changes is important to ensure that you can afford higher payments if the rate adjusts upward.

ARMs typically offer lower initial interest rates compared to fixed-rate mortgages, which can lead to lower initial monthly payments. This can be beneficial if you plan to sell or refinance before the adjustable period begins.

The initial period is when the interest rate on an ARM is fixed. After this period, the rate adjusts at regular intervals. For example, a 7/1 ARM has a fixed rate for the first seven years and then adjusts once every 12 months.

ATV Loans

AutoPay is a convenient service that automatically withdraws your loan payment each month from your People Driven Credit Union checking or savings account. It helps you stay on track, avoid late fees, and may even qualify you for our ¹Special Loan Rate Discount.

To enroll in AutoPay, please call us at 248-263-4100 and a representative will assist you with setup.

Our ¹Special Loan Rate Discount offers a 0.25% APR reduction when you set up automatic payments (AutoPay) for your loan from a People Driven Credit Union checking or savings account. This discount is already included in the “as low as” rate advertised.

To enroll in AutoPay and receive the discount, please call us at 248-263-4100. A representative will assist you in setting up monthly automatic withdrawals from your PDCU account.

Note: The discount is available only for eligible loans with AutoPay set up from a PDCU account. Terms and conditions may apply.

Absolutely. We offer financing options for both new and pre-owned ATVs. Terms and rates may vary based on the vehicle’s condition and age.

Yes, our pre-approval process lets you know your borrowing power before you start shopping for your perfect ATV.

Our ATV loans cover a variety of all-terrain vehicles designed to enhance your off-road adventures, including, ATVs, UTVs (Utility Task Vehicles), side-by-sides (sxs) four-wheelers, quad bikes, recreational off-highway vehicles (ROVs), and multipurpose off-highway utility vehicle (MOHUV).

Have something in mind and wondering if PDCU will finance it? Call us as 248-463-4100.

Our application process often provides pre-approval decisions quickly, and final approval typically takes just a few days once all documentation is submitted.

Yes, enrolling in autopay may qualify you for a rate discount, reducing the overall cost of your loan. Check with our team for current promotional details.

A down payment may be needed, depending on your credit profile, the value of the vehicle or watercraft, and the specific loan structure. While not always required, a down payment can lower your monthly payments and the total amount of interest paid. Our representatives will guide you through the requirements. Call 248-263-4100 to speak with a PDCU loan officer.

Loan terms are flexible and can be tailored to fit your financial situation. At People Driven Credit Union, loan terms for recreational vehicles such as ATVs, motorcycles, boats, snowmobiles, and campers generally range from 12 to 180 months. Longer terms can lower monthly payments but may result in higher total interest paid.

Interest rates vary based on factors like your credit score, loan term, and the age of the vehicle or watercraft. People Driven Credit Union offers competitive rates to make financing accessible and affordable for our members. Call 248-263-4100 to speak with a PDCU loan officer about the loan rate you can expect.

Auto Loan Help

Yes, enrolling in autopay may qualify you for a rate discount, reducing the overall cost of your loan. Check with our team for current promotional details.

Missing a payment can result in late fees and negatively affect your credit score. Repeated missed payments may lead to vehicle repossession. It’s important to contact People Driven Credit Union as soon as possible if you anticipate any issues making payments on your loan from PDCU.

People Driven Credit Union members can pay off an auto loan anytime with no penalty.

To check the status of your loan application, contact People Driven Credit Union at 248-263-4100 during business hours or reach out to your assigned loan specialist if you have their contact information. Be ready to verify your identity and share details such as your name, member number, or application number so we can review your application with you.

When you check your status, it is also a good idea to ask whether any additional documents or information are needed to keep your application moving. Review times can vary based on the loan type and the information required, so contacting us directly is the best way to get the most current update on your application.

Yes. People Driven Credit Union offers a Skip A Payment option for eligible loans during qualifying periods. If you qualify, you may be able to skip one loan payment per calendar year for a $35 processing fee.

Who may qualify

To be eligible, you must be a member in good standing, have no prior extensions in the current calendar year, and have the $35 fee available for withdrawal. Some loan types are excluded, including Fresh Start Auto Loans, Lines of Credit, Mortgages, Commercial Loans, and Credit Cards.

How to request it

You can request Skip A Payment through the MyPDCU app, through online banking, or by completing the Authorization Form and submitting it to a branch or mailing it to:

Skip-A-Payment

People Driven Credit Union

24333 Lahser Road

Southfield, MI 48033

Important to know

Finance charges will continue to accrue during the skipped month, and skipping a payment may extend the term of your loan. If you have automatic payments set up through PDCU or another financial institution, you will need to stop those payments for the skipped month and restart them afterward. Your request and fee must be received at least one business day before the payment is due.

Need help?

If you have questions about eligibility or how to request Skip A Payment, call 248-263-4100 or 844-700-7328 during business hours.

Auto Loan Refinancing

Refinancing replaces your current auto loan with a new one—usually with a different lender, to secure a lower rate, adjust your monthly payment, or change your term. PDCU pays off your existing lender and you make payments to PDCU going forward.

Common reasons include: your credit score has improved, market rates have dropped, your original rate was high, you want a lower monthly payment, you want to pay off faster with a shorter term, or you need to add/remove a co-signer.

For the most current APRs, please visit our Loan Rates page. Terms are available up to 72 months for eligible vehicles. Your approved rate and term will depend on factors like creditworthiness, amount financed, and the vehicle’s age, value, and condition, and are subject to change at any time.

Cars, trucks, SUVs, and vans that are new or used (5 years old or newer).

No. This offer is for loans refinanced from another lender or for new loans only.

Yes. Loans must close within 30 days of application to qualify for promotional terms.

We’ll run a hard credit inquiry during the application, which may have a small, temporary impact on your score.

Savings depend on your new rate, term, and remaining balance. Many members save by lowering their APR, shortening the term, or both. We’re happy to run the numbers for you before you commit.

Yes. You can choose a term (up to 96 months) that fits your budget and goals—either lowering your payment or paying off sooner.

A valid ID and SSN, proof of income, your current loan statement/10-day payoff, and vehicle info (VIN, mileage, year/make/model). We’ll let you know if anything else is needed.

Auto Loans

Fees include:

- Application fees

- Origination fees

- Title and registration fees

- Prepayment penalties (if applicable)

Interest rates vary based on factors like your credit score, the loan term, the lender, and the vehicle’s age. It’s a good idea to shop around for the best rate and check if you qualify for any discounts.

Start by looking at your full monthly budget, not just the vehicle payment. You should also consider insurance, fuel, maintenance, and other regular expenses. Choosing a payment that feels comfortable, not tight, can help you stay on track after the excitement of buying the vehicle wears off.

Today’s auto loan rates:

Auto Loan Rates (for new vehicles)

Auto loan rates for cars, trucks, SUVs, & vans five years old or newer:

|

Term (Months) |

≤36 |

37-48 |

49-60 |

61-72 |

73-84 |

96 |

|---|---|---|---|---|---|---|

|

APR* as low as¹ |

4.74% | 4.74% | 4.74% | 4.74% | 5.24% | 5.74% |

|

Rates Effective as of: |

||||||

Auto Loan Rates (for used vehicles)

Auto loan rates for used cars, trucks, SUVs, & vans older than five years. Add 3.00% to the applicable rate on loans with collateral that is 10 years old or older.

|

Term (Months) |

≤36 |

37-48 |

49-60 |

61-72 |

73-84 |

96 |

|

APR* as low as¹ |

4.74% | 4.74% | 4.74% | 4.74% | 5.24% | 5.74% |

|

Rates Effective as of: |

||||||

Disclosures

*APR = Annual Percentage Rate: The actual APR and loan term is subject to approval and may be determined upon the borrower’s creditworthiness, the amount borrowed, and the type, value, age, and condition of the collateral offered to secure the loan (when applicable). Rates are effective as of today and are subject to change.

¹Special Loan Rate Discount: Benefit from a .25% reduction when enrolling in our autopay service, which is included in the “as low as” rate advertised. The discount is available to those who setup autopay of their monthly loan payment from a People Driven Credit Union checking or savings account.

People Driven Credit Union is an Equal Housing Opportunity Lender NMLS #776727

All other trademarks are the property of their respective owners.

AutoPay is a convenient service that automatically withdraws your loan payment each month from your People Driven Credit Union checking or savings account. It helps you stay on track, avoid late fees, and may even qualify you for our ¹Special Loan Rate Discount.

To enroll in AutoPay, please call us at 248-263-4100 and a representative will assist you with setup.

Our ¹Special Loan Rate Discount offers a 0.25% APR reduction when you set up automatic payments (AutoPay) for your loan from a People Driven Credit Union checking or savings account. This discount is already included in the “as low as” rate advertised.

To enroll in AutoPay and receive the discount, please call us at 248-263-4100. A representative will assist you in setting up monthly automatic withdrawals from your PDCU account.

Note: The discount is available only for eligible loans with AutoPay set up from a PDCU account. Terms and conditions may apply.

Yes, enrolling in autopay may qualify you for a rate discount, reducing the overall cost of your loan. Check with our team for current promotional details.

Your credit score plays a big role in determining your loan’s interest rate and terms. Borrowers with higher credit scores typically qualify for lower interest rates, while those with lower credit scores may face higher rates.

- New auto loans apply to brand-new cars, trucks, vans, and vehicles five years old or newer. They often have lower interest rates because new cars typically have better collateral value.

- Used auto loans apply to pre-owned vehicles older than five years; interest rates may be slightly higher since used cars have less value over time.

An auto loan is a type of financing that allows you to borrow money to purchase a vehicle. The loan is secured by the vehicle itself, meaning the lender can repossess the vehicle if you fail to repay the loan.

Auto Loans Exotic Cars

That part’s easy. You can apply online, give us a call, or visit a branch to connect with a loan specialist. We’ll answer your questions, review your options, and help you decide whether an Exotic Car Loan is a good fit.

In some cases, yes. If you already own an exotic car and want to explore refinancing—whether to lower your payment or adjust your term—reach out to us. We’ll review your current loan and the vehicle details to see if we can help.

Down payment requirements can depend on the vehicle, the purchase price, and your overall financial situation. A larger down payment can sometimes improve your approval chances or lower your monthly payment. We’ll look at your full picture and discuss what makes sense for your situation.

Available terms can vary based on the vehicle, loan amount, and your credit profile. Longer terms may offer a lower monthly payment, while shorter terms may help you pay less in total interest. We’ll review options with you so you can choose a term that fits your goals.

We may be able to finance exotic vehicles purchased from either reputable dealers or private sellers, depending on the situation. The documentation required can differ, so it’s best to contact us before you sign anything so we can walk you through what’s needed.

In many cases, yes. Pre-owned exotic vehicles are often eligible, but condition, mileage, age, and value all matter. We may request additional documentation, inspections, or valuation information to confirm eligibility.

Exotic cars generally include high-end, specialty, performance, or collectible vehicles that fall outside typical mass-market models. This may include supercars, rare or limited-edition sports cars, certain luxury models, and some classic or specialty vehicles. If you’re not sure whether your dream car qualifies, ask us—we’ll review it with you.

Our ¹Special Loan Rate Discount offers a 0.25% APR reduction when you set up automatic payments (AutoPay) for your loan from a People Driven Credit Union checking or savings account. This discount is already included in the “as low as” rate advertised.

To enroll in AutoPay and receive the discount, please call us at 248-263-4100. A representative will assist you in setting up monthly automatic withdrawals from your PDCU account.

Note: The discount is available only for eligible loans with AutoPay set up from a PDCU account. Terms and conditions may apply.

Auto Loans: Indirect

Log in to Online Banking to update AutoPay or one-time payments. For ACH from another bank, submit a new EFT authorization.

Check your Welcome Letter for your exact due date and monthly payment amount. If you need a copy, contact us.

Give your employer PDCU’s routing number #272484988 and your account number. You can find your account number in Online Banking or on your membership documents.

People Driven Credit Union’s routing number is 272484988.

You may need this routing number to set up direct deposit, schedule automatic payments, make ACH transfers, or link your People Driven Credit Union account to another financial institution.

This routing number is the same for all People Driven Credit Union members. If you need help with wire transfers, please review our Wiring Instructions or contact us directly for assistance.

Boat Loans

AutoPay is a convenient service that automatically withdraws your loan payment each month from your People Driven Credit Union checking or savings account. It helps you stay on track, avoid late fees, and may even qualify you for our ¹Special Loan Rate Discount.

To enroll in AutoPay, please call us at 248-263-4100 and a representative will assist you with setup.

Our ¹Special Loan Rate Discount offers a 0.25% APR reduction when you set up automatic payments (AutoPay) for your loan from a People Driven Credit Union checking or savings account. This discount is already included in the “as low as” rate advertised.

To enroll in AutoPay and receive the discount, please call us at 248-263-4100. A representative will assist you in setting up monthly automatic withdrawals from your PDCU account.

Note: The discount is available only for eligible loans with AutoPay set up from a PDCU account. Terms and conditions may apply.

You’ll generally need proof of income, a look at your credit history, and details about the watercraft you wish to finance. Our team is here to help every step of the way. For more information or personalized assistance, please contact a People Driven Credit Union representative at 248-263-4100.

Our application process often provides pre-approval decisions quickly, and final approval typically takes just a few days once all documentation is submitted.

Yes, enrolling in autopay may qualify you for a rate discount, reducing the overall cost of your loan. Check with our team for current promotional details.

A down payment may be needed, depending on your credit profile, the value of the vehicle or watercraft, and the specific loan structure. While not always required, a down payment can lower your monthly payments and the total amount of interest paid. Our representatives will guide you through the requirements. Call 248-263-4100 to speak with a PDCU loan officer.

Loan terms are flexible and can be tailored to fit your financial situation. At People Driven Credit Union, loan terms for recreational vehicles such as ATVs, motorcycles, boats, snowmobiles, and campers generally range from 12 to 180 months. Longer terms can lower monthly payments but may result in higher total interest paid.

Yes, PDCU finances both new and pre-owned watercraft. Rates and terms may differ, so our team can help you find the best option based on your needs.

Absolutely. Our pre-approval process gives you a clear idea of your borrowing power before you start shopping, simplifying your purchasing journey.

Interest rates vary based on factors like your credit score, loan term, and the age of the vehicle or watercraft. People Driven Credit Union offers competitive rates to make financing accessible and affordable for our members. Call 248-263-4100 to speak with a PDCU loan officer about the loan rate you can expect.

Business

People Driven Credit Union stays actively involved with the Southeast Michigan Chamber of Commerce. We partner on events, sponsor programs, and work alongside other local businesses to help support and grow Michigan companies.

Business Account Help

If you were a former Community Alliance Credit Union business member and used software such as QuickBooks, Quicken, or Mint, your business accounts may have required a connection update after the merger with People Driven Credit Union. The original conversion period took place in March 2023, so these instructions apply only to that legacy transition process.

Original conversion dates

March 10, 2023: Final transaction download and backup before conversion.

March 13, 2023: Deactivate and reactivate your online banking connection using People Driven Credit Union settings.

Conversion guides

QuickBooks Desktop Conversion Instructions

QuickBooks Online Conversion Instructions

Quicken Conversion Instructions

Mint Conversion Information

What to do now

If you are still having trouble with a legacy business account connection or accounting software setup, contact People Driven Credit Union for help reviewing your current account access and connection settings.

Need help?

Call 844-700-7328 or 248-263-4100 during business hours, or visit Contact Business Services.

You can view your eStatements by signing in to online banking or by using the MyPDCU app. Once you are signed in, open the Statements or Documents section and select the statement you want to view or download.

How to view your eStatements online

Log in to online banking, click on the eStatements tab, choose the month or statement period you need, and open the file. You can usually view the statement on screen or download it as a PDF for your records.

How to view your eStatements in the app

Open the MyPDCU app, tap eStatements, select the account if needed, and choose the statement you want to open.

Need help?

If you cannot find a statement or need help accessing your eStatements, call 844-700-7328 during business hours. Statement history may vary by account and retention policies.

To close your People Driven Credit Union account, contact us directly by phone or visit a branch. We will verify your identity, review your account status, and help you complete the closure process.

How to close your account

Call 248-263-4100 or visit a branch to request account closure. Before the account is closed, make sure you review your current balance, pending payments, automatic withdrawals, and direct deposits. You should also transfer or withdraw any remaining funds and request confirmation once the account has been closed.

Important to know

Account closures are not handled online. If you receive direct deposit or have recurring payments tied to the account, be sure to update those with your employer, benefits provider, or billing companies before closing the account.

Need help?

If you have questions about closing your account, call 248-263-4100 during business hours, or visit a branch for assistance.

CashBack

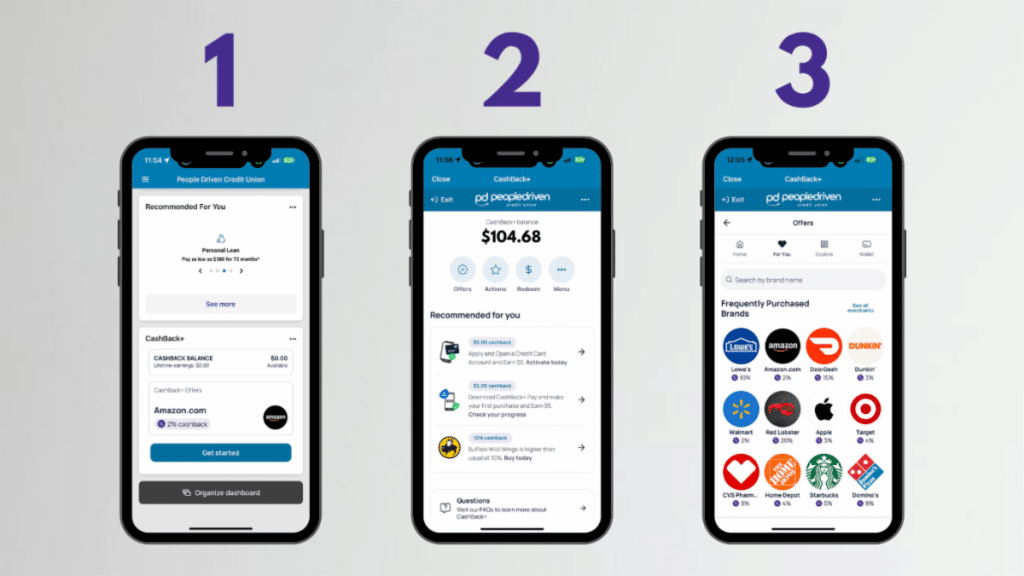

How to get started with Cashback+

- Open Your MyPDCU Mobile App

Open your MyPDCU Mile App, and locate the CashBack+ widget on your dashboard. Click Get Started. - Choose the “Offers” Button

From the four buttons below your balance, select “Offers.” - Explore the Offers!

Spend some time checking out all of the available offers for your favorite places to shop and eat!

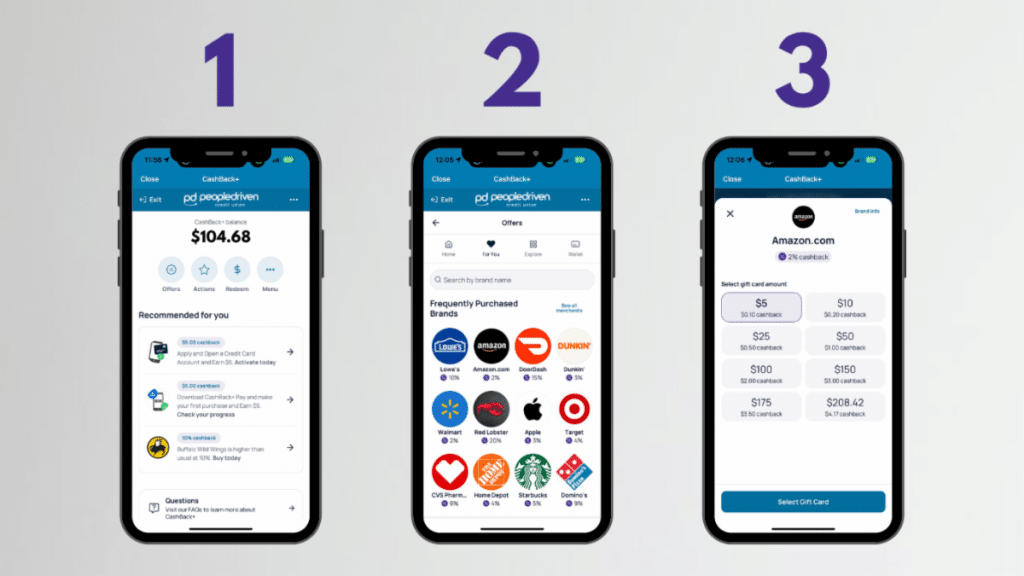

Choosing Offers

- Navigate to your CashBack+ Widget

Once inside the portal, click Offers. - Select Your Retail Brand of Choice

Scroll or search for the retail brand you want to purchase with to see what the brand’s current cash-back offer is at the time. - Purchase the Gift Card to Make a Purchase

You will purchase a gift card to cover the amount of the purchase you are attempting to make. This gift card has been purchased and stored in your CashBack+ Wallet. You can choose to use this immediately or store it in your wallet for later use.

Using CashBack+ Wallet

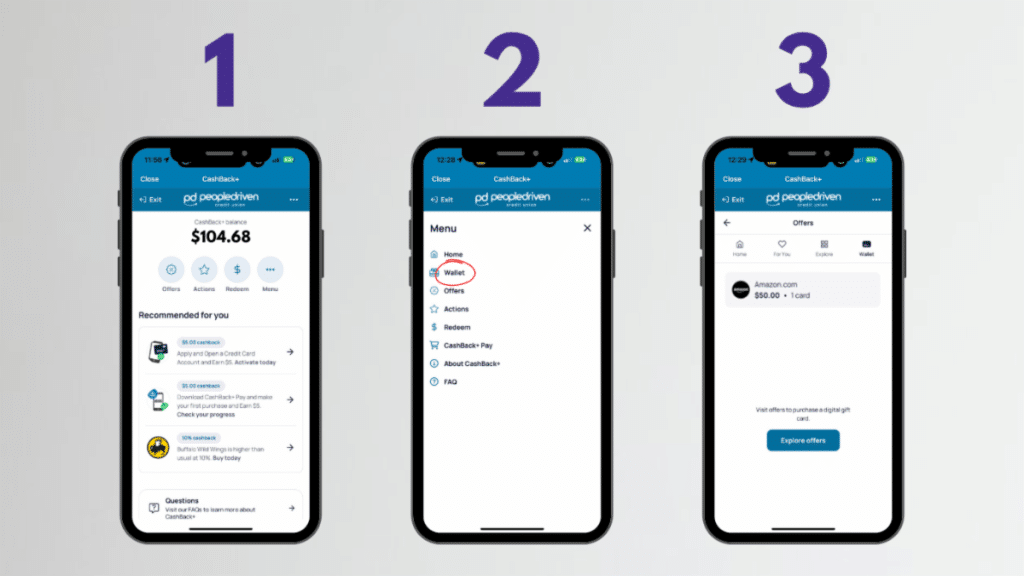

- Navigate to your CashBack+ Widget

Once inside the portal, click More. - An Action Menu Will Appear

From the menu, select Wallet. - Select the Gift Card You Wish to Use

To use the card, click on the Gift Card you want to use from your wallet. Select Shop Now. This will direct you to the company website. Alternatively, you can use the gift card code by copying and pasting it at checkout online.

For more information about Cashback+, read our blog post, “How to Use CashBack+“.

CashBack+ is a comprehensive cashback rewards program available within your PDCU online banking. It offers personalized cashback deals, rewards for purchases, and bonus cashback for everyday banking actions.

You earn cashback by purchasing digital gift cards through Offers, using the CashBack+ Pay app at checkout, or completing certain actions such as making debit card transactions or enrolling in eStatements.

- Offers are proactive purchases of digital gift cards you plan to use later.

- Pay allows you to earn cashback on purchases you’re already making through the convenient CashBack+ Pay app.

Example: When shopping at Walmart, enter your purchase total into CashBack+ Pay, generate a barcode, scan it at checkout, and immediately earn cash back.

Digital gift cards are delivered via email and stored securely in your CashBack+ Wallet accessible within your mobile app or online banking.

Gift cards do not expire for at least five years from the purchase date.

No, there’s no limit! Earn as much cashback as you want, whenever you want.

CashBack+ is available for Android and iPhone users, as well as via the Chrome browser on desktops.

Cashback is earned instantly and visible in your CashBack+ account immediately after completing your purchase.

Yes, CashBack+ Pay is device-specific and provides enhanced security compared to traditional card transactions.

CD

You must be the child’s parent, grandparent, or legal guardian to open and manage an account. As the joint account holder, you’ll be able to set up account alerts, parental controls, online access and more.

It’s a bank account that can help your kids and teens learn to manage money. Our youth accounts come with both a checking and saving account where parents are able to set up alerts and limits. Plus, you can guide your child through real-world experiences like using an ATM. There’s a minimum of $5 for the first deposit – and no monthly service fee.

Our youth accounts are for ages 0-17.

A 16-month CD (Certificate of Deposit) is a type of savings account offered by banks and credit unions. Here are the key characteristics:

- Fixed Term: It has a maturity period of nine months, during which the deposited money is locked in.

- Interest Rate: Typically offers a fixed interest rate generally higher than regular savings accounts.

- Minimum Deposit: Often requires a minimum deposit amount to open the account.

- Early Withdrawal Penalty: If you withdraw the funds before the 16-month term ends, you usually incur a penalty, a portion of the interest earned, or a specified fee.

- FDIC Insured: In the United States, CDs from credit unions are usually insured by the National Credit Union Administration (NCUA) up to $250,000 per depositor per credit union.

A 16-month CD can be a good option if you have a specific short-term savings goal and want to earn a higher interest rate without taking on much risk.

A 16-month CD works as follows:

- Opening the CD: You deposit a lump sum of money into the CD account. The amount often needs to meet the bank or credit union’s minimum deposit requirement.

- Fixed Term: The money is committed to the CD for a fixed term of nine months. During this period, you cannot add to or withdraw from the principal amount without incurring penalties.

- Interest Rate: The bank or credit union pays you a fixed interest rate on the deposited amount for the entire term. This rate is usually higher than that of a regular savings account because the bank can use your money for a predictable period.

- Interest Accumulation: Interest is typically compounded and credited to your account at regular intervals, such as monthly or quarterly.

- Maturity: At the end of the 16-month term, the CD matures. You then have a few options:

- Withdraw the funds: You can take out your initial deposit plus the interest earned.

- Renew the CD: You can roll over the funds into a new CD, either for the same term or a different one, possibly at a new interest rate.

- Transfer the funds: You can transfer the money to another account.

- Early Withdrawal Penalty: If you need to access the money before the 16-month term ends, you will likely face an early withdrawal penalty. This penalty varies by institution but generally involves forfeiting a portion of the interest earned.

- FDIC/NCUA Insurance: If the CD is held at a bank, it is insured by the FDIC (Federal Deposit Insurance Corporation) up to $250,000 per depositor per bank. If held at a credit union, it is insured by the NCUA (National Credit Union Administration) with the same coverage limits.

A 16-month CD can be a suitable option for short-term savings goals, offering a balance between earning a higher interest rate and having your money tied up for a relatively short period.

Yes, your money is safe in a 16-month CD. At People Driven Credit Union, our CDs are insured by the NCUA (National Credit Union Administration) up to $250,000 per depositor.

APY stands for Annual Percentage Yield. It is a measure of the total amount of interest earned on an account based on the interest rate and the frequency of compounding over a year. APY is a useful metric for comparing the annual earnings on different savings products, such as savings accounts, CDs, and money market accounts, because it standardizes the effect of compounding.

Key Points About APY

- Includes Compounding: APY accounts for how often interest is compounded (e.g., daily, monthly, quarterly), which can significantly affect the total interest earned over time.

- Comparison Tool: APY provides a standard way to compare the annual interest earnings of different savings products, regardless of how frequently interest is compounded.

- Formula: The formula for calculating APY is:

APY = (1 + r/n)^n - 1

where r is the nominal interest rate (expressed as a decimal), and n is the number of compounding periods per year.

- Higher APY: A higher APY indicates that you will earn more interest on your money over a year, assuming the same principal amount.

Example

For example, if a savings account offers an interest rate of 5% compounded monthly, the APY would be higher than 5% due to the effect of monthly compounding. This makes APY a useful metric for comparing the real return on different financial products.

You will receive a notice in the mail 30 days before the maturity date of your CD.

Once the initial deposit has been made funds cannot be added to the CD until maturity. Once the CD matures you may add funds if you wish to renew the CD.

Although a CD is not necessarily liquid, it is considered one of the safest investments available. The longer CD you have, the higher the rate is going to be. There are no fees for the Certificate of Deposit, and you earn interest based on the balance in the CD.

Certificate of Deposit Help

You can view your eStatements by signing in to online banking or by using the MyPDCU app. Once you are signed in, open the Statements or Documents section and select the statement you want to view or download.

How to view your eStatements online

Log in to online banking, click on the eStatements tab, choose the month or statement period you need, and open the file. You can usually view the statement on screen or download it as a PDF for your records.

How to view your eStatements in the app

Open the MyPDCU app, tap eStatements, select the account if needed, and choose the statement you want to open.

Need help?

If you cannot find a statement or need help accessing your eStatements, call 844-700-7328 during business hours. Statement history may vary by account and retention policies.

Checking

Overdraft Protection Transfer is an optional service offered by People Driven Credit Union that allows eligible members to link a savings account to a checking account. If there are insufficient funds in your checking account to cover a transaction, available funds from the linked savings account may be automatically transferred to cover the shortfall.

This service is designed to reduce the likelihood of declined transactions or returned items due to insufficient funds (NSF).

Key details:

- Transfers occur only if sufficient funds are available in the linked account.

- A per-transfer fee may apply.

- Funds are transferred in the exact amount needed to cover the transaction, subject to available balance and transfer limits.

Overdraft Protection Transfers are subject to account eligibility, terms, and limitations. Not all accounts qualify. Transfers from savings accounts are subject to regulatory and policy limits. For full details, contact a PDCU representative.

Courtesy Pay is a discretionary overdraft service available to eligible People Driven Credit Union members with checking accounts in good standing. If you do not have enough available funds to cover a transaction, we may choose to pay it for you up to the applicable limit.

What Courtesy Pay may cover

Courtesy Pay may apply to checks, ACH transactions such as electronic bill payments, and recurring debit card payments. If you want Courtesy Pay to apply to everyday debit card transactions, such as point-of-sale purchases or ATM transactions, you must first opt in.

Important to know

Courtesy Pay is not a line of credit, and it is not guaranteed. Eligibility depends on your account history and other factors, and we may decline to pay a transaction even if your account is eligible. If we do pay an overdraft item, a fee may apply for each transaction. Any negative balance must be repaid promptly, and repeated or excessive use may result in the service being suspended or discontinued.

Need help or want to opt in?

To ask about Courtesy Pay, request opt-in coverage for everyday debit card transactions, or review current fees, contact us.

People Driven Credit Union offers several overdraft options for checking accounts, including Overdraft Protection Transfer, Courtesy Pay for eligible accounts, or the choice to have transactions declined if you do not want overdraft coverage.

Overdraft Protection Transfer

You can link your Basic Checking Account to a PDCU savings account. If you have available funds in savings, money can transfer automatically to help cover a transaction. A transfer fee may apply..

Courtesy Pay

Courtesy Pay is available for eligible accounts in good standing. If approved at our discretion, it may help cover overdrafts for checks, ACH payments, and recurring debit card transactions up to the applicable limit. Opt-in is required if you want Courtesy Pay to apply to everyday debit card transactions. A fee may apply for each overdraft item that is paid.

Courtesy Pay is a discretionary service, not a guarantee. To remain eligible, you must bring your account back to a positive balance within 30 days. Other restrictions may apply.

No overdraft service

You can also choose not to use overdraft services. If a transaction exceeds your available balance, it may be declined and no overdraft fee will apply.

Need help choosing an option?

To ask questions about your overdraft options or update your preferences, contact our Member Services team.

Gone are the days when you had to visit a branch to deposit your checks. With People Driven Credit Union’s mobile check deposit service, managing your finances becomes a breeze. This technology, known as remote deposit capture, lets you deposit checks from anywhere by simply snapping a picture with your device.

How Mobile Check Deposit Works:

- Set the Stage: Place your check against a dark background to ensure all details are captured clearly due to the contrast.

- Sign and Specify: Endorse the back of the check and write “For Mobile Deposit Only to PDCU” along with your clear signature and account number to streamline processing.

- Open the MyPDCU App: Log in and select “Deposits.”

- Enter the Check Details: Enter the check amount and select the account where you want to deposit it.

- Capture the Check Images: Place the front of the check within the phone’s frame and tap the screen to capture an image. Repeat for the back of the check.

- Verify the Deposit: Check your transaction history in the app to ensure the deposit was successful.

- Secure Disposal: After confirming the deposit, cut up the check to secure your personal information. Dispose of the pieces separately.

The check will be deposited into the requested account and become available according to our standard check processing timeline. Past deposits can be viewed in the app.

For additional details, please visit our website at peopledrivencu.org/amazing or contact us if you have questions.

Embrace simplicity and security with our digital banking solutions. At People Driven Credit Union, we’re here to make your financial management effortless.

Need to send money to your People Driven Credit Union account or start a wire transfer or Electronic Funds Transfer request? Use the information below to help route funds correctly and learn how to begin your request securely.

Important: Wire transfers can move quickly and may be difficult or impossible to reverse once sent. Always verify wiring instructions directly with People Driven Credit Union before sending funds.

Incoming Wire Instructions

Use the following information when wiring funds to a People Driven Credit Union account.

Wire To

Alloya Corporate Federal Credit Union

184 Shuman Blvd, Suite 400

Naperville, IL 60563

ABA/Routing Number: 271987635

Credit To

People Driven Credit Union

24333 Lahser Road

Southfield, MI 48033

Account Number: 272484988

Final Credit Information

Include the following member information so funds can be credited correctly:

- Member’s name

- Member’s PDCU account number

- Member’s address

- Account type, such as savings or checking

Start a Wire Transfer or Electronic Funds Transfer Request

To begin a wire transfer or Electronic Funds Transfer request, please complete the Electronic Funds Transfer form. After you submit the form, a People Driven Credit Union team member will contact you to verify your request and complete the next steps.

Submitting the form does not complete or send the transfer. It starts the request process. PDCU will contact you before the transfer is completed.

Complete the Electronic Funds Transfer Form

Before You Send a Wire

Before sending funds, verify the wire instructions directly with People Driven Credit Union. Do not rely only on instructions received by email, text message, or a phone number provided in a message.

Call us at 844-700-PDCU (7328) if you have questions or need to confirm wiring instructions.

Electronic Fund Transfer Disclosure

You have rights under the Federal Electronic Fund Transfer Act, also known as Regulation E. For questions or to report an unauthorized Electronic Funds Transfer, call us immediately at 248-263-4100.

- Report errors within 60 days of statement receipt.

- We will investigate and correct errors within 45 days.

For complete details, please review our Electronic Funds Transfer Disclosures.

Wiring Instructions: Frequently Asked Questions

Wire transfers can move quickly and may be difficult or impossible to reverse once sent. Always confirm the routing number, account number, final credit information, and dollar amount directly with People Driven Credit Union before sending funds.

You can start the request process by completing the Electronic Funds Transfer form. After the form is submitted, People Driven Credit Union will contact you to verify the request and complete the next steps. Submitting the form does not complete or send the transfer.

The final credit information should include the member’s name, PDCU account number, address, and account type, such as savings or checking.

Wire fraud often happens when a scammer impersonates a trusted organization, title company, real estate professional, financial institution, or other known contact. They may send fake wiring instructions by email, phone, or text to redirect funds to an account they control.

Treat wiring instructions as unverified until you confirm them directly with People Driven Credit Union. Call us using the phone number listed on our official website, not a number provided in an email, text message, or voicemail about the transfer.

Contact the sending financial institution immediately and request a wire recall. Then call People Driven Credit Union at 248-263-4100 so we can document the situation and assist where possible.

People Driven Credit Union will not send unsolicited changes to wiring instructions by email or text. If you receive changed wiring instructions, stop and call us directly at 844-700-PDCU (7328) before taking action.

People Driven Credit Union’s routing number is 272484988. For incoming wires, the ABA routing number listed for Alloya Corporate Federal Credit Union is 271987635.

Need Help?

If you have questions about wiring instructions, an Electronic Funds Transfer request, or suspected wire fraud, contact People Driven Credit Union before sending funds.

Call 844-700-PDCU (7328) or visit our Contact Us page.

People Driven Credit Union’s checking accounts do not require a minimum balance and do not have monthly maintenance fees.

If you are opening a new account and are not already a member, a Membership Share Savings Account is required to establish membership. That account requires a $5 deposit.

PDCU checking accounts also include convenient features such as a Visa Debit Card, online banking, mobile banking, bill pay, and mobile check deposit. If you have questions about opening a checking account, call 844-700-7328 during business hours.

To make a mobile deposit, log in to the MyPDCU app or online banking

Before you submit your deposit

Sign the back of the check and write “For Mobile Deposit Only at PDCU” along with your PDCU account number. Make sure the photos are clear and complete so your deposit can be processed correctly. Deposits over $2,500 will be reviewed by the credit union and may not appear in your account right away. The mobile deposit check limit is $25,000, and all deposits are subject to holds.

After you submit your deposit

Keep the original check in a secure place for 7 business days after the deposit and verify that the funds have been credited to your account. After that, mark the check “VOID” and destroy it, preferably by shredding it. If you have questions about mobile deposit, call 844-700-7328.

You can help avoid overdrafts by monitoring your available balance, setting account alerts, reviewing pending transactions, and choosing the overdraft option that best fits your needs.

Set account alerts

Use the MyPDCU app or online banking to set low-balance and transaction alerts so you know when your balance is getting low or when activity posts to your account. Alerts can help you act before a transaction causes an overdraft.

Review your available balance

Check your account regularly and pay attention to pending purchases, ACH payments, and other scheduled transactions. Reviewing your available balance instead of only your current balance can help you avoid spending money that is already committed.

Choose the overdraft option that fits you

People Driven Credit Union offers Overdraft Protection Transfer from linked savings, which currently costs $3 per transfer, and Courtesy Pay for eligible accounts, which currently has a $30 fee per item paid. Courtesy Pay is discretionary and not guaranteed. You can also choose to opt out of overdraft services so transactions that exceed your available balance may be declined without an overdraft fee.

Need help?

If you want help reviewing your overdraft settings or choosing an option, call 248-263-4100 or 844-700-7328 during business hours.

Order Checks in the Online Banking Portal

Log in to online banking at my.peopledrivencu.org. Click on your checking account. Scroll about halfway down the page to find the “Check Reorder” link. Click it and follow the prompts to complete your order.

Order Checks in the MyPDCU Mobile App

Open the MyPDCU app on your phone. Go to your checking account details. Look for the Check Reorder option. Confirm your details and submit the order. It is quick and easy.

Reorder Checks from Our Website

Click the Reorder Checks link to our partner, Harland Clark. Enter our routing #272484988. Enter your account number (the full 14 digits) and your Account/Home zip code. On the next screen, enter your address, phone number, and email address. Then select your preferred branch. and complete your order.

Or just ask our Team, “How do I order checks?”

Call us at 248-263-4100 during business hours. You can also visit any branch in Livonia, Southfield, Warren, Ypsilanti, or Romeo.

Helpful hints for when you plan on ordering checks

- Double-check your shipping address before you submit the order.

- Reorder checks when you have about 15-20 checks left to avoid running out.

- Watch for delivery timing updates after you submit your order.

- Contact us at 248-263-4100 if you need help ordering checks.

People Driven Credit Union offers checking account options for members who want easy access to their money. Our Basic Checking Account is designed for everyday spending and digital banking. We also offer Money Market Plus and High-Yield Money Market Accounts for members who want to earn more than a standard savings account while still keeping their funds accessible.

Account options to consider